Our commitment to responsible practices touches many aspects of our business, enabling the Group to drive positive impacts through our products and services. Our approach infuses trust into our brand and industry, promotes sustainable growth, and positively influences the communities we serve.

Supporting the Transition to a Low-carbon Economy

Answering the call on financed emissions

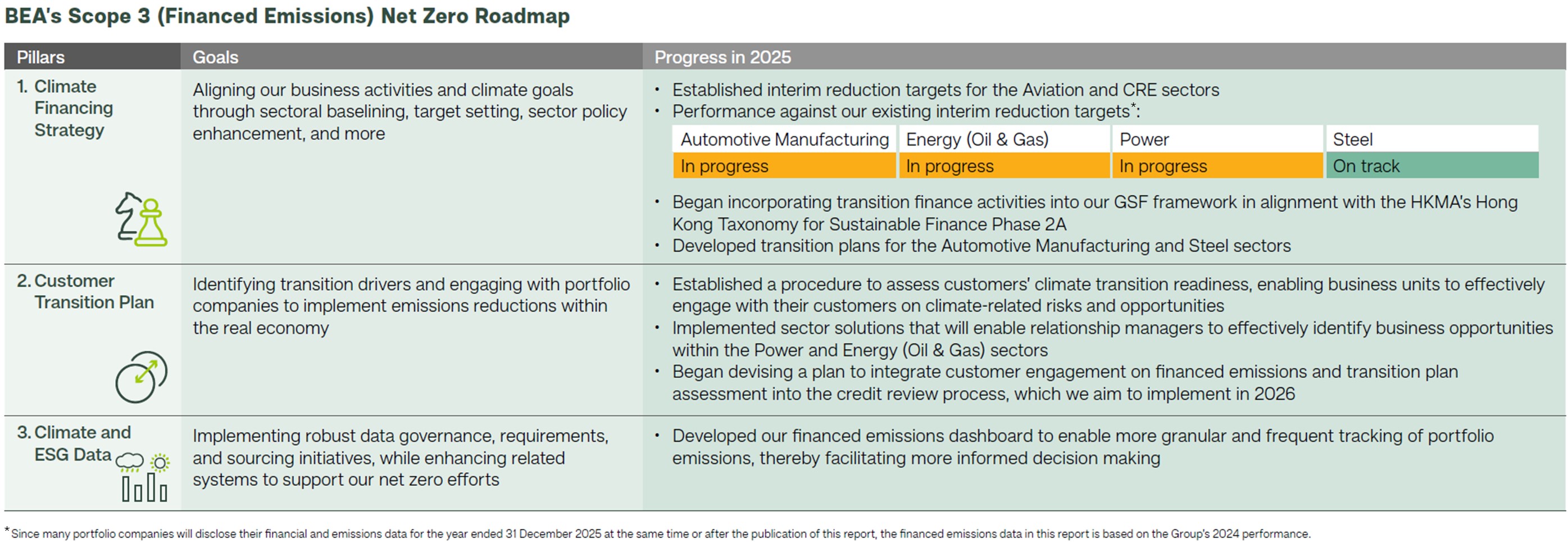

Financed emissions comprise more than 99% of the Group’s total emissions. Recognising the important role BEA plays as a provider of capital in the fight against climate change to fulfil the aims of the Paris Agreement, we are advancing the goal of achieving net zero financed emissions by 2050. Guided by the three pillars of our Scope 3 Net Zero Roadmap, we made significant progress in 2025.

In late 2025, BEA became the first bank headquartered in Hong Kong to join the Principles for Responsible Banking (PRB) under the United Nations Environment Programme Finance initiative. The PRB enables us to contribute to industry discussions on defining frameworks to help banks align strategies and practices to further the goals of the Paris Agreement.

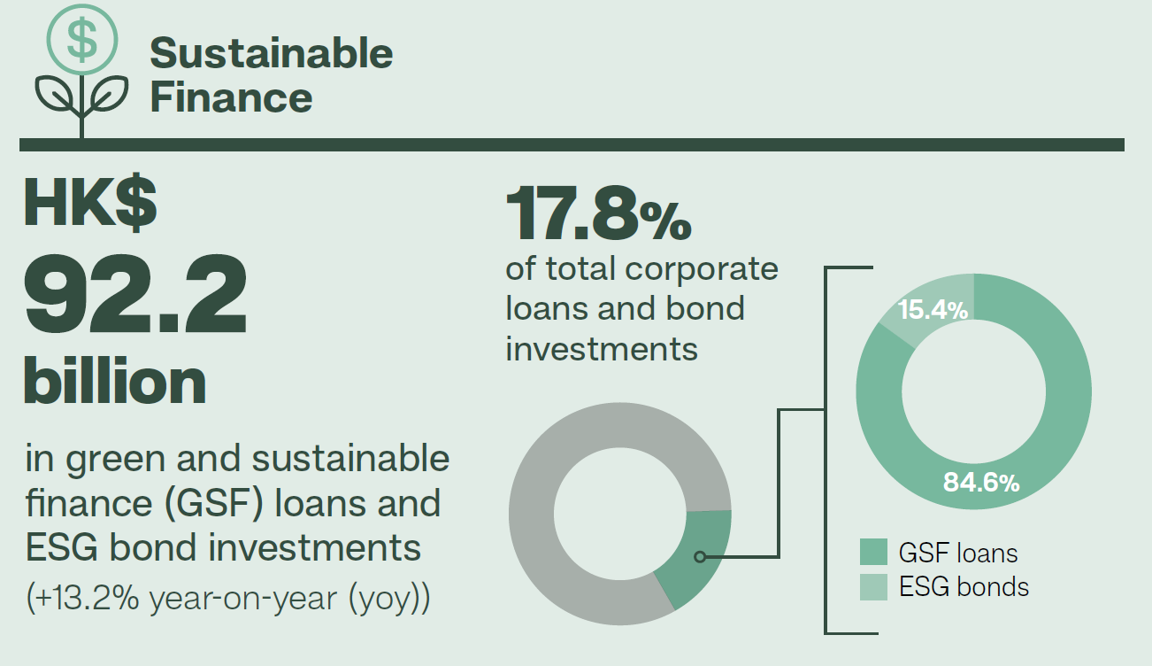

Growing our green and sustainable finance (GSF) business

We have developed and rolled out sustainability-focused products and services across the Group to support our customers on their own sustainability journeys. For instance, we offer GSF lending solutions for corporate customers such as green and sustainability-linked loans.

Sustainability is also embedded in our debt investment strategy through ESG bond investments. We are directing capital towards projects and businesses of investee companies that have climate ambitions and visions aligned with ours.

In 2025, we continued to identify new opportunities and transitioned existing investments to ESG-labelled bonds. We also actively monitored and managed our carbon-intensive sector portfolios. To support the Group’s net zero financed emissions goal, we replenished or switched our bond holdings to include companies with lower emissions profiles and credible transition strategies, where feasible.

Managing our ESG and climate-related risk proactively

Our robust Enterprise Risk Management (ERM) framework effectively identifies and manages potential risks, including ESG and climate-related risks, in alignment with the requirements established by the Hong Kong Monetary Authority (HKMA).

We integrate climate risk assessment into our credit decision-making and review processes. The designated Relationship Manager or Treasury Market Credit Manager evaluates the counterparty’s exposure to physical and transition risks, alongside their strategic plan for transitioning to a low-carbon economy, for the applications they manage. This evaluation is independently reviewed by a Credit Assessor before escalation to the Credit Committee. Comprising the Deputy Chief Executive, Group Chief Risk Officer, and other senior executives, the Credit Committee maintains oversight of identified climate-related risks and holds ultimate authority for credit approval decisions.

As we continue to invest in GSF opportunities, we are aware of the significant risks posed by greenwashing. To this end, in 2022, BEA has established a GSF framework with consistent, technically sound definitions and methodologies as well as tools to identify and assess the environmental and social impacts of the projects we finance to mitigate greenwashing risk in our GSF portfolio. It has been designed to cover a range of financial solutions provided by the Group, including loans, bonds, working capital finance, trade finance, and bank guarantees.

As part of our GSF framework, a List of Prohibited Lending specifies transactions or activities that BEA will not knowingly extend financing to. These transactions and activities are:

- Development, manufacturing and trading of firearms

- Production or trading of wildlife products in violation of the Convention on International Trade in Endangered Species of Wild Fauna and Flora

- Activities that would adversely impact areas that have been designated as UNESCO World Heritage Sites

- Activities involving exploitation of children and human trafficking

- Activities resulting in degradation and/or destruction of:

- any biodiversity value areas; or High Conservation Value, High Carbon Stock forests or peatlands, wetlands designated under the Ramsar Convention on Wetlands of International Importance, or

- the natural sites designated by UNESCO as the World Heritage Site

- Unauthorised logging or deforestation

- Plantation operations that use fire to clear the land in preparation for planting

- Activities that are directly related to the exploitation, development, or production of oil and gas within the Arctic Circle

- Mountaintop-removal coal mining

- Operations which practice shark finning or trade in shark fin products

- Illegal Unreported and Unregulated fishing; this also includes operations which practice drift net fishing, deep sea bottom trawling or fishing with the use of explosives or cyanide

Additionally, our new product approval procedure requires business units to consult the Sustainability Department and ESG Risk & Oversight Department on ESG-themed products and services. This helps ensure products and services support proper ESG causes and subject matter expertise is applied to identify and address potential greenwashing risks before they materialise.

To accelerate efforts in achieving our net zero targets, we have launched the Coal Phase-out Policy (the Policy) which covers our main business activities in loan financing and bond investment. We will no longer provide financing dedicated to the development of new coal-fired power plants, thermal coal mines or capacity expansion. Furthermore, we are committed to phasing out our financing dedicated to existing coal-fired power plants and thermal coal mines, as well as our exposure to companies whose main business is thermal coal power generation or mining, by 2030 in Organisation for Economic Cooperation and Development (OECD) countries and 2040 in non-OECD countries. The Group will continue to offer green and transition financing to support the sector's transition.

For details on how we manage climate-related risks, please refer to the Climate-related Risk and Resilience section of our latest ESG Report.

Promoting Responsible Products and Services

Our commitment to delivering responsible products and services is built on two core principles: addressing evolving customer needs and ensuring strict compliance with local regulations. BEA is also a signatory to the HKMA’s Treat Customers Fairly (TCF) Charter.

To help ensure ongoing compliance with the TCF Charter and continually improve our products and services, all employees, including those in customer-facing positions, are required to complete an annual TCF training, covering topics such as risk information sharing, responsible product offerings, marketing practices, and best practices for complaint handling.

Developing cutting-edge, inclusive products and services

Our banking solutions are designed to meet the diverse needs of different customer segments, from providing financing for local businesses and small and medium enterprises (SMEs) to offering cutting-edge platforms for digitally savvy customers and donation collection services for non-governmental organisations (NGOs).

In 2025, we introduced two new tailored loan products for SMEs as part of our Enterprise Easy Fund series, including an Energy Efficiency Loan that aims to support SMEs in their green transition, empowering them to capture business opportunities while advancing sustainable practices that help Hong Kong achieve its carbon neutrality target by 2050.

Meeting cross-boundary financial needs

We partnered with Guangzhou Rural Commercial Bank Co., Ltd. to expand its Cross-Boundary Wealth Management Connect (WMC) 2.0 business in 2025, enabling more qualified investors in the GBA to seize southbound cross-boundary investment opportunities, including over 280 eligible fund products.

Eligible GBA residents who successfully open a Southbound account can instantly benefit from BEA’s advanced digital banking services (including BEA Mobile and BEA Online) and access a comprehensive range of wealth management and investment services, along with the latest market insights.

Assessing the financial capabilities of customers

We carefully evaluate each customer’s financial capabilities before offering any product, service, or advice. In line with our responsible lending policy, we offer loan restructuring schemes for retail customers facing financial hardship. For unsecured products and credit cards, customers can apply for the Facility Re-arrangement Scheme via our customer hotline or by mail. For secured mortgage lending, customers may request adjustments to repayment terms—including changes to loan tenor, installment amounts, or repayment frequency—through our online application form or via a paper form.

Debt collection and recovery

Our debt recovery procedures, as set out in our Credit Risk Management Manual, define the roles and responsibilities of the dedicated department and Debt Recovery Units. Each Debt Recovery Unit maintains an operation manual that sets out clear workflow for collecting and recovering debts from retail and corporate customers, aiming to ensure fair treatment with a proportionate and consistent approach for the collection and recovery of outstanding amounts.

To ensure relevant staff are well-prepared for various debt collection scenarios, we provide regular training on loan recovery enforcements. We also conduct an annual forum on credit risk management for involved personnel.

Providing service excellence

Our quest to ensure a positive customer experience is guided by ISO 10002:2018 Quality Management: Customer Satisfaction Standard. Applying this standard helps us monitor trends, identify external and internal issues, and eliminate causes of complaints leading to continual improvement in our operations, products, and services.

Procedures have been established to set out defined roles and responsibilities, and procedures and timeline in handling customer complaints. We have also implemented supplementary guidelines specific to financial products, including selling of FX Accumulators for hedging purpose, and purchase and sale of investment products. Our Complaint Officer oversees complaint handling, and makes a final decision on case allocation and substantiation, while designated complaint officers of relevant departments are responsible for handling relevant complaints.

Quarterly complaint management reports, which include key customer complaint statistics, are sent to Senior Management and department heads, with key performance indicators reported to the Board and Remuneration Committee through the Bank Culture Dashboard.

Insights derived from complaint analysis and customer feedback are systematically reviewed and integrated into our product review and new product approval processes, ensuring alignment with customer needs and regulatory expectations.

Promoting financial literacy and inclusion

To foster financial inclusion and education while serving our customers, we continuously explore ways to connect with different demographics and markets we serve. By tailoring our strategies, we aim to ensure our services not only meet the needs of all customers but also empower them with the knowledge and tools to thrive in today's digital banking world.

Building on this commitment, one of our primary goals is to make our banking services easily accessible to everyone. Across our branch network, we have taken tangible steps, such as installing specially designed teller counters and ATMs to assist customers with wheelchair needs, visual or auditory impairments, and other challenges. Additionally, recognising the unique needs of individuals with hearing impairments, we have introduced a conversational live chat service on the BEA website and BEA Mobile, offering an inclusive and seamless customer experience.

As part of our inclusivity efforts, we strive to bridge the digital divide by helping customers aged 60 and above in their adoption of digital banking services. We have implemented high-contrast interfaces and optimised, legible typography on the BEA Mobile app, ensuring seamless readability and navigation. Following these efforts, we were recognised by Hong Kong Internet Registration Corporation Limited by winning the Triple Gold Award in the Digital Accessibility Recognition Scheme 2024/25 (Mobile App Stream). Since the launch of the revamped BEA Mobile app, we have intensified promotional efforts among this group with encouraging feedback.

To allow customers in remote areas or those with mobility constraints to access core banking services conveniently, we also introduced a fully digital Mobile Account Opening journey featuring simplified steps, clear instructions, and remote identity verification. This significantly lowers onboarding barriers for these customers, eliminating the need to visit a physical branch.

Through sharing financial knowledge and guidance with our senior customers, we also promote financial literacy. For instance, in 2025, we hosted a Bank Smart Seminar at our Shatin Branch in Hong Kong, where Personal Banking representatives provided guidance on securing digital transactions and safeguarding deposits and savings, reaching 40 customers. In the UK, we co-organised a UK Taxation, Education, and Fraud Prevention Seminar with accounting and education partners and hosted a Fraud Prevention Workshop for our customers as part of a local Chinese community event held in Birmingham, reaching over 150 customers.

For more information on other financial literacy initiatives and community programmes, please refer to Responsible Citizen.

Safeguarding Cybersecurity and Data Privacy

The foundation of cybersecurity and data privacy governance at BEA rests on the "Three Lines of Defence" risk management model. This model helps the Bank capture and monitor cybersecurity and data risks, while clarifying the roles and responsibilities of committees involved. The effectiveness of the cybersecurity and data protection governance framework and control processes is independently and regularly assessed by the Internal Audit Division following a risk-based approach or by a qualified external assessor.

On the data privacy front, BEA fully complies with personal data privacy laws in all jurisdictions where it operates, including the Hong Kong Personal Data (Privacy) Ordinance, the UK General Data Protection Regulation, and the Chinese Mainland Personal Information Protection Law. Comprehensive policies and guidelines have been established to help safeguard our customers’ data and personal information privacy.

Our Group Privacy Policy sets out general personal data protection principles that apply across BEA Group members, helping to ensure that personal data is handled with care and confidentiality, and with respect for individual rights. Meanwhile, our Privacy Policy Statement outlines our approach to data collection and retention, in line with regulatory requirements. Our Personal Information Collection (Customers) Statement also outlines that, in relation to account data, customers can request deletion of such data from relevant databases, subject to applicable legal and regulatory requirements.

While the rapid pace of digitalisation presents unparalleled opportunities for growth, it also necessitates robust cybersecurity measures to safeguard systems and data within an evolving threat landscape. Our Information Security Policy provides a comprehensive framework detailing the infrastructure, organisational structure, and our employees' responsibilities essential to managing information security. In addition, the Policy clearly sets out the information security requirements for third parties. It highlights the Bank’s commitment to continuously improving its information security systems, ensuring integrity and protection of data, and vigilance and responsiveness to related threats.

We apply a "privacy-by-design" approach to our digital channel developments to strengthen cybersecurity and protect customer data. We embed data protection controls into our product architecture before launch. These include robust device security frameworks to securely anchor accounts to authorised devices, continuous customer education through security tips and step-by-step demo guides on BEA Online and BEA Mobile, and application-level safeguards such as end-to-end encryption, secure session management, and data masking for sensitive personal information. These measures help ensure customer privacy is protected throughout every digital interaction.

Upholding Business Ethics and Integrity

Upholding high ethical standards is essential for the long-term success and sustainability of our business. The Bank’s Code of Conduct addresses a wide range of topics, including corruption and bribery, discrimination, sexual harassment, use/confidentiality of information, conflicts of interest, money laundering, insider trading/dealing, and more. Each year, all staff members are required to read the latest version of the Code, declaring their understanding and confirming compliance with it and the policies embedded therein.

We also conduct mandatory training on the Code of Conduct to all employees, including part-time and contract staff. This training covers the Whistleblowing Policy and Procedure, which outlines available reporting channels for addressing unethical business practices.

BEA is also a signatory of the Banking Industry Integrity Charter (Integrity Charter) introduced by the Independent Commission Against Corruption (ICAC). The Integrity Charter aims to combat and prevent corruption through public-private partnership, assisting banks to enhance integrity management systems while strengthening corruption prevention awareness and related capabilities.

By signing the Integrity Charter, BEA is strengthening its sound bank culture and reiterating its commitment to the Bank's Code of Conduct. We have appointed an integrity officer to assist the Bank in the oversight and implementation of good governance. We also provide integrity training to staff and promptly report suspected corruption, fraud and other illicit activities to the ICAC or other law enforcement agencies promptly.

For more details about the Integrity Charter, please visit ICAC’s website.

To learn more about our ESG initiatives and recent updates, please refer to Responsible Business section of our latest ESG Report.