Life Insurance - Savings and Retirement Income

Underwritten by AIA International Limited (Incorporated in Bermuda with limited liability)

SEIZE CURRENCY OPPORTUNITIES AND POTENTIAL RETURNS

Global Power Multi-Currency Plan offers a choice of up to 7 currencies, helping you achieve long-term wealth accumulation and potentially attractive returns, with the flexibility to change policy currency.

Capture global opportunities and enjoy long-term wealth accumulation

Build up long-lasting prosperity with smart wealth planning to meet your ever-changing needs

Global Power Multi-Currency Plan offers a choice of up to 7 currencies for long-term wealth accumulation with potentially high returns, and the option to enjoy the advantages of changing policy currency in an evolving world. Whether you want to build your child’s education fund, reach your retirement goals or plan your legacy for your loved ones, you can achieve your financial goals with the help of Global Power Multi-Currency Plan, and access your cash flexibly as different needs arise.

Plan Highlights

Up to 7 currencies for your selection

Under the Global Power Series, Global Power Multi-Currency Plan is a participating whole-life insurance plan that covers the entire lifespan of the insured, who is the person protected under the policy. You can select from up to 7 currencies for your policy, which include Renminbi (RMB), British pound sterling (GBP), US dollars (US$), Australian dollars (AUD), Canadian dollars (CAD), HK dollars (HK$) and Macau pataca (MOP; only for policies issued in Macacu), each offering different policy returns.

The broad choice of currency lets you plan ahead by choosing the currency that will best suit your upcoming plans, whether as future funds for your children’s education, enjoying life after retirement or other opportunities overseas.

Change your policy currency with the Currency Exchange Option

As your needs may change from one life stage to the next, Global Power Multi-Currency Plan’s Currency Exchange Option lets you capture ever-evolving opportunities in a dynamic world, access the advantages of global currencies and continue accumulating wealth with extra financial flexibility.

The Currency Exchange Option allows you to change your policy currency to another currency as listed above, by exchanging your plan to the latest plan under the Global Power Series while maintaining the policy duration and without requiring a medical examination. The option is available once per policy year after the end of the 3rd policy year. Please refer to Cover at a glance and Key Product Risks for further details.

Accumulate wealth with a one-time or 5-year premium payment term

Global Power Multi-Currency Plan can help you achieve guaranteed and potential gains. To suit your long-term wealth accumulation needs and your budget, you can choose a one-time premium payment term or a 5-year premium payment term to help meet your financial goals.

Global Power Multi-Currency Plan offers guaranteed cash value. We will also distribute the profit generated from the product group of this participating whole-life insurance plan by declaring non-guaranteed Reversionary Bonus and Terminal Bonus to your policy at least once per year starting from the end of the 3rd policy year. These comprise:

- Reversionary Bonus: A non-guaranteed bonus, the face value of which forms a permanent addition to your policy once it is declared. Its cash value may be cashed out or left to accumulate in your policy throughout its duration.

- Terminal Bonus: A non-cumulative, non-guaranteed bonus, the amount of which is valid until the next declaration. It is payable under the death benefit and upon policy surrender and termination.

If the worst should happen and the insured passes away, according to the death benefit calculation, we will pay the face values of any Reversionary Bonus accumulated and Terminal Bonus to the person whom you select in your policy as the beneficiary.

Otherwise, upon the surrender or termination of your policy, we will pay any cash values that may have accumulated on any Reversionary Bonus, and the cash value of the Terminal Bonus under the policy.

Realise potential returns with the Bonus Lock-in Option

Through the Bonus Lock-in Option, Global Power Multi-Currency Plan enables you to realise potential returns by transferring the latest cash values of the Reversionary Bonus and Terminal Bonus into a Bonus Lock-in Account to earn interest at a non-guaranteed rate. This is available once per policy year, starting from the end of the 15th policy year.

To provide further flexibility for your financial needs throughout various life stages, you can also withdraw cash from the Bonus Lock-in Account anytime without reducing the principal amount of your policy.

Flexible withdrawal to meet your changing needs

With Global Power Multi-Currency Plan, you can withdraw your policy values in one go to realise your dreams or make withdrawals flexibly according to your changing needs in the future.

Upon request, you can withdraw part of the guaranteed cash value and the non-guaranteed cash values of the Reversionary Bonus and Terminal Bonus. However, this will reduce the future values of your policy. After withdrawal, the principal amount of the policy and the total premiums paid or one-time premium paid (as applicable) for the basic plan under the death benefit may be reduced.

To meet your changing needs in the future, you may choose to withdraw all cash values in the policy. Upon such withdrawal, you will receive the sum of the guaranteed cash values, non-guaranteed cash values of the Reversionary Bonus and Terminal Bonus and any remaining balance of the Bonus Lock-in Account (if applicable) and your policy will be terminated.

We will deduct all outstanding debt under the policy before we make any payments for your withdrawal.

Change of Insured Option and Contingent Insured Option to pass your legacy across future generations an unlimited number of times

During the lifetime of the current insured and after the end of the 1st policy year, the Change of Insured Option allows you to change the insured to another loved one, in whom you and the beneficiary have insurable interest. That way, the value of your policy can be inherited by later generations, helping you pass on your wealth with extra flexibility.

With the Contingent Insured Option, during the lifetime of the current insured, you can designate another loved one as a contingent insured, in whom you and the beneficiary have insurable interest. There is no limit on the number of times you can designate, modify or remove a contingent insured, as long as it is done during the lifetime of the current insured, but you may only have one contingent insured per policy at any time during the benefit term. Upon the passing of the current insured, the contingent insured may become the new insured without affecting your policy values so as to protect your legacy for the next generation.

You may change the insured under the Change of Insured Option and/or the Contingent Insured Option as many times as you wish, subject to our approval.

Your choice of settlement option if the worst should happen

If the insured passes away and no contingent insured has become the new insured, we will pay the death benefit to the person whom you select in your policy as beneficiary.

The death benefit will include the higher of:

- 105% of the total premiums paid or one-time premium paid (as applicable) for the basic plan; and

- the sum of the guaranteed cash value and the face values of any Reversionary Bonus and any Terminal Bonus in the policy;

plus any remaining balance of the Bonus Lock-in Account (if applicable).

We will deduct all outstanding debt under the policy before we make the payment to the beneficiary.

To ease your financial burden during unforeseen challenges, Global Power Multi-Currency Plan offers extra protection through an accidental death benefit, which is equal to the total premiums paid or one-time premium paid for your basic plan (as applicable). This is paid in addition to the above death benefit if the insured passes away due to a covered accident within the first year of the policy.

Apart from a lump sum payment, the death benefit and accidental death benefit can alternatively be paid to the beneficiary in regular instalments by applying the death benefit settlement option during the lifetime of the insured, according to the specific benefit amounts to be paid at regular intervals chosen by you.

Rewards for academic excellence

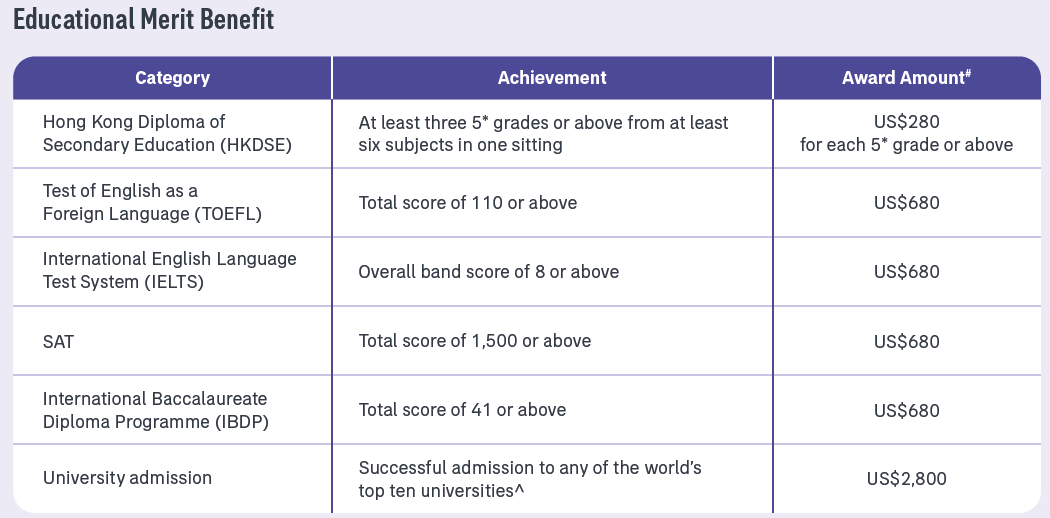

To motivate the insured to strive for academic excellence, we will reward academic achievements by offering the Educational Merit Benefit. Once the policy has been in force for at least 1 year, if the insured obtains any one of the following achievements before the age of 25, Global Power Multi-Currency Plan will pay the corresponding award amount while the policy is in force.

The Educational Merit Benefit will only be paid for one of the following categories once per policy.

# If the policy is issued in a currency other than US$, the award amount would be available in the respective policy currency and the prevailing exchange rate will be used to calculate the above amounts.

^ The ranking is based on a source as determined by us from time to time. For the latest details, please click here.

The Educational Merit Benefit will terminate if you have claimed for the award amount in respect of any one insured. With respect to the same insured under all Global Power Multi-Currency Plan policies, the Educational Merit Benefit is only payable once per life.

If you have changed the insured of the policy through the Change of Insured Option or Contingent Insured Option, Global Power Multi-Currency Plan will only pay the Educational Merit Benefit when the new insured achieves the required achievements at least 1 year after the change of insured and before age 25 of the new insured. We reserve the right to change the terms and conditions of the Educational Merit Benefit from time to time without further notice.

Delay premium payments in case of unemployment for 5-year premium payment policies

Unemployment may cause a significant impact on your finances. To help ease your financial burden while keeping the insured protected, you may claim for the Unemployment Benefit if you are laid off and become involuntarily unemployed during the premium payment term of the basic plan.

Once your application is approved, the grace period for late premium payment will be extended from 31 days up to 365 days. The Unemployment Benefit is available once per policy. Please refer to the Note for Unemployment Benefit for further details.

Add-on cover for policies with a 5-year premium payment term

If you opt for a 5-year premium payment term, you may select an add-on plan under which we will waive the future premiums for Global Power Multi-Currency Plan if the insured becomes totally and permanently disabled before the age of 60, providing support in the face of unfortunate circumstances.

In addition, you may also select the Payor Benefit Rider, under which we will waive the future premiums for the basic plan until the insured reaches the age of 25 should you pass away or suffer total and permanent disability before the age of 60.

All add-on plans are subject to additional premiums, underwriting and exclusions. All benefits under add-on plans will be terminated when your Global Power Multi-Currency Plan policy terminates.

Cover at a glance

| Premium Payment Term | One-time | 5-year |

| Insured's Age at Application | 15 days - age 80 | 15 days - age 75 |

| Benefit Term | Whole life | |

| Policy Currency | RMB / GBP / US$ / AUD / CAD / HK$ / MOP (only for policies issued in Macau) | |

| Principal Amount | For calculation of the premium and relevant policy values only and will not be payable as the death benefit | |

| Minimum One-time / Annual Premium | RMB45,000 / GBP4,500 / US$7,500 / AUD7,500 / CAD7,500/ HK$56,250 / MOP56,250 | RMB12,000 / GBP1,200 / US$2,000 / AUD2,000 / CAD2,000 / HK$15,000 / MOP15,000 |

| Currency Exchange Option |

The Currency Exchange Option allows you to change your policy currency to another currency selected by you (including Renminbi (RMB), British pound sterling (GBP), US dollars (US$), Australian dollars (AUD), Canadian dollars (CAD), HK dollars (HK$) and Macau pataca (MOP; only for policies issued in Macau)), by exchanging your plan to the latest plan under the Global Power Series, while maintaining the policy duration and without requiring a medical examination. Before you apply

Once your application is approved

|

|

| Non-Guaranteed Reversionary Bonus and Terminal Bonus |

The following non-guaranteed bonuses will be declared to your policy at least once per year starting from the end of the 3rd policy year: Reversionary Bonus

Terminal Bonus

|

|

| Bonus Lock-in Option |

Within 30 days after the end of each policy year, starting from the end of the 15th policy year, you may apply to exercise the Bonus Lock-in Option once per policy year. Transfer of Lock-in Amount You can decide on what percentage of the Reversionary Bonus and Terminal Bonus to transfer, subject to the following rules: - The percentages of the Reversionary Bonus and Terminal Bonus transferred into your Bonus Lock-in Account must be identical to each other. - The percentages cannot be less than 10% or more than 70% (minimum and maximum percentages are subject to our prevailing rules and regulations) and the Lock-in Amount is subject to a minimum amount that is determined by us from time to time.

Value of the Bonus Lock-in Account

|

|

| Surrender Benefit |

The surrender benefit will include:

We will deduct all outstanding debt under the policy before we make the payment. |

|

| Change of Insured Option |

You may exercise the change of insured under the Change of Insured Option as many times as you wish, subject to our approval. At the time of applying to exercise the Change of Insured Option

After the change of insured

|

|

| Contingent Insured Option |

You may exercise the change of insured under the Contingent Insured Option as many times as you wish, subject to our approval. At the time of designating the Contingent Insured

Upon the passing of the current insured

Upon the contingent insured becoming the new insured

|

|

| Death Benefit |

The death benefit will include the higher of:

plus any remaining balance of the Bonus Lock-in Account (if applicable). We will deduct all outstanding debt under the policy before we make the payment to the beneficiary. |

|

| Accidental Death Benefit | In addition to the death benefit, if the insured passes away due to a covered accident within the first year of the policy, the accidental death benefit will equal the total premiums paid or one-time premium paid (as applicable) for the basic plan. The maximum aggregate amount of the accidental death benefit with respect to the same insured under all Global Power Multi-Currency Plan polices is RMB600,000 / GBP60,000 / US$100,000 / AUD100,000 / CAD100,000 / HK$750,000 / MOP750,000 and the benefit payable under each policy will be prorated according to its total premiums paid or one-time premium paid (as applicable) for the basic plan. | |

| Death Benefit Settlement Option |

* If the policy is issued in a currency other than US$, the amount would be available in the respective policy currency and the prevailing exchange rate willbe used to calculate the above amount. |

|

| Policy Loan |

|

|

| Underwriting | No medical examination is required for your application as long as the total annual premiums or one-time premium payment (as applicable) does not exceed the aggregate limit set for each insured, subject to our prevailing rules and regulations. | |

Important Information

The brochure does not contain the full terms and conditions of the policy. It is not, and does not form part of, a contract of insurance and is designed to provide an overview of the key features of this product. The precise terms and conditions of this plan are specified in the policy contract. Please refer to the policy contract for the definitions of capitalised terms, and the exact and complete terms and conditions of cover. In case you want to read policy contract sample before making an application, you can obtain a copy from AIA. The brochure should be read along with the illustrative document (if any) and other relevant marketing materials, which include additional information and important considerations about this product. We would like to remind you to review the relevant product materials provided to you and seek independent professional advice if necessary.

This plan can be only purchased through Bank of East Asia as a basic plan.

The brochure is for distribution in Hong Kong / Macau only.

“AIA”, “the Company”, “We”, “our” or “us” herein refers to AIA International Limited (Incorporated in Bermuda with limited liability).

Effective from 1 January 2018, all policy owners are required to pay a levy on each premium payment made for both new and in-force Hong Kong policies to the Insurance Authority (IA). For levy details, please visit our website at www.aia.com.hk/useful-information-ia-en or IA’s website at www.ia.org.hk.

Bonus Philosophy

This is a participating insurance plan designed to be held long term. Your premiums will be invested in a variety of assets according to our investment strategy, with the cost of policy benefits (such as charges to support guarantees) and expenses deducted as appropriate from premiums or assets. Your policy can share the divisible surplus (if any) from related product groups determined by us. A very significant proportion of divisible surplus arising from actual experience gains and losses from related product groups will be shared with policy owners. We aim to ensure a fair sharing of profits between policy owners and shareholders, and among different groups of policy owners.

Future investment performance is unpredictable. Through our smoothing process, we aim to deliver more stable Reversionary Bonus and Terminal Bonus payments, by spreading out the gains and losses over a longer period of time. Stable Reversionary Bonus and Terminal Bonus payments will ease your financial planning.

We will review and determine the Reversionary Bonus and Terminal Bonus amounts to be payable to policy owners at least once per year. The actual Reversionary Bonus and Terminal Bonus declared may be different from those illustrated in any product information provided (e.g. benefit illustrations). If there are any changes in the actual Reversionary Bonus and Terminal Bonus against the illustration or in the projected future Reversionary Bonus and Terminal Bonus, such changes will be reflected in the policy anniversary statement.

A committee has been set up to provide independent advice on the determination of the Reversionary Bonus and Terminal Bonus amounts to the Board of the Company. The committee is comprised of members from different control functions or departments within the organisation both at AIA Group level as well as Hong Kong local level, such as office of the Chief Executive, legal, compliance, finance and risk management. Each member of the committee will exercise due care, diligence and skill in the performance of his or her duties as a member. The committee will utilise the knowledge, experience, and perspectives of each individual member to assist the Board in the discharge of its duty to make independent decision and to manage the risk of conflict of interests, in order to ensure fair treatment between policy owners and shareholders, and among different groups of policy owners. The actual Reversionary Bonus and Terminal Bonus, which are recommended by the Appointed Actuary, will be decided upon the deliberation of the committee and finally approved by the Board of Directors of the Company, including one or more Independent Non-Executive Directors.

To determine the Reversionary Bonus and Terminal Bonus of the policy, we consider both past experiences and the future outlook for all the factors including, but not limited to, the following:

Investment returns: include interest earnings, dividends and any changes in the market value of the product’s backing assets depending on the asset allocation adopted for the product, investment returns could be affected by fluctuations in interest income (both interest earnings and the outlook for interest rates) and various market risks, including credit spread and default risk, fluctuations in equity prices, property prices and foreign exchange currency fluctuation of the backing asset against the policy currency.

Claims: include the cost of providing death benefits and other insured benefits under the product(s).

Surrenders: include policy surrenders, partial surrenders and policy lapses; and the corresponding impact on the investments backing the product(s).

Expenses: include both expenses directly related to the policy (e.g. commission, underwriting, issue and premium collection expenses) and indirect expenses allocated to the product group (e.g. general administrative costs).

Some participating products (if applicable) allow the policyholder to leave annual dividends, guaranteed and nonguaranteed cash payments, guaranteed and non-guaranteed incomes, guaranteed and non-guaranteed annuity payments with us, potentially earning interest at a non-guaranteed interest rate. To determine such interest rate, we consider the returns on the pool of assets in which the annual dividends, guaranteed and non-guaranteed cash payments, guaranteed and non-guaranteed incomes, guaranteed and nonguaranteed annuity payments are invested with reference to the past experience and future outlook. This pool of assets is segregated from other investments of the Company and may include bonds and other fixed income instruments.

For dividend & bonus philosophy and dividend / bonus history, please visit AIA's website at www.aia.com.hk/en/dividend-philosophy-history.html.

Investment Philosophy, Policy and Strategy

Our investment philosophy is to deliver stable returns in line with the product’s investment objectives and AIA’s business and financial objectives.

Our investment policy aims to achieve the targeted long-term investment results and minimise volatility in investment returns over time. It also aims to control and diversify risk exposures, maintain adequate liquidity and manage the assets with respect to the liabilities.

Our current long-term target strategy is to allocate assets attributed to this product as follows:

| Asset Class | Target Asset Mix |

| Bonds and other fixed income instruments | 25% 100% |

| Equity-like assets | 0% - 75% |

Our investment strategy is to actively manage the investment portfolio i.e.: adjust the asset mix in response to the external market conditions. The proportion of equity-like assets would be lower when interest rate level is low and would be even lower than the long-term target strategy so to protect the guaranteed liability and to minimise volatility in investment returns over time, and vice versa when interest rate is high.

The bonds and other fixed income instruments predominantly include government and corporate bonds, and are mainly invested in the geographic region of the United States, Canada, the United Kingdom and Asia-Pacific (excluding Japan). Equity-like assets may include listed equity, mutual funds and direct / indirect investment in commercial / residential properties, which are mainly invested in Asia. Equity-like assets may also include private equity, which is typically invested in the United States. Returns of equity-like assets are generally more volatile than bonds and other fixed income instruments. Subject to our investment policy, material amount of derivatives may be utilised to manage our investment risk exposure and for matching between assets and liabilities.

Our currency strategy is to minimise currency mismatches. For bonds or other fixed income instruments, our current practice is to currency-match their bond purchases with the underlying policy denomination on best-efforts basis (e.g. US Dollar assets will be used to support US Dollar liabilities). Subject to market availability and opportunity, bonds may be invested in currency other than the underlying policy denomination and currency swap will be used to minimise the currency risks. Currently assets are mainly invested in US dollars / the denominated currency. For equity-like assets, currency exposure depends on the geographic location of the underlying investment where the selection is done according to our investment philosophy, investment policy and mandate.

We will pool the investment returns from other long term insurance products (excluding investment linked assurance schemes and pension schemes) together with this participating insurance plan for determining the actual investment and the return will subsequently be allocated with reference to the target asset mix of the respective participating products. Actual investments (e.g. geographical mix, currency mix) would depend on market opportunities at the time of purchase. Hence it may differ from the target asset mix.

The investment strategy may be subject to change depending on the market conditions and economic outlook. Should there be any material changes in the investment strategy, we will inform policy owners of the changes, with underlying reasons and impact to the policies.

Key Product Risks

- You should pay premium(s) on time and according to the selected premium payment schedule. If you stop paying the premium before completion of the premium payment term, you may surrender the policy, otherwise, the premium will be covered by a loan taken out on the policy automatically. When the loan balance exceeds the sum of guaranteed cash value and cash value of Reversionary Bonus (if any) of the basic plan, the policy will terminate and you will lose the cover. The surrender value of the policy will be used to repay the loan balance, and we will refund any remaining value.

- The plan may make certain portion of its investment in equity- like assets. Returns of equity-like assets are generally more volatile than bonds and other fixed income instruments, you should note the target asset mix of the product as disclosed in this product brochure, which will affect the bonus on the product. The savings component of the plan is subject to risks and possible loss. Should you surrender the policy early, you may receive an amount considerably less than the total amount of premiums paid.

- For one-time premium payment policies, they are subject to higher investment return volatility and thus are expected to have higher volatility on the bonuses payable, as compared to policies with a 5-year premium payment term which can benefit from cost averaging effect.

-

You may request for the termination of your policy by notifying us in written notice. Also, we will terminate your policy and you / the insured will lose the cover when one of the following happens:

• the insured passes away, except when the contingent insured becomes the new insured;

• you do not pay the premium within 31 days (or 365 days under Unemployment Benefit) of the due date and the policy has no cash value (Only applicable for a 5-year premium payment policy); or

• the outstanding debt exceeds the guaranteed cash value plus the non-guaranteed cash value of the Reversionary Bonus (if any) of the policy. - We underwrite the plan and you are subject to our credit risk. If we are unable to satisfy the financial obligations of the policy, you may lose your premium paid and benefits.

- You are subject to exchange rate risks for plans denominated in currencies other than the local currency. Exchange rates fluctuate from time to time. You may suffer a loss of your benefit values and the subsequent premium payments (if any) may be higher than your initial premium payment as a result of exchange rate fluctuations. You should consider the exchange rate risks and decide whether to take such risks.

- In case if the currency is changed under the Currency Exchange Option, the adjustments on policy value may be significant (either positive or negative) and the amount after exercising the Currency Exchange Option may be considerably less than the total amount of premiums paid. Any future premiums will be adjusted if the Currency Exchange Option is exercised within the premium payment term. The approval of the Currency Exchange Option's application and the availability of currency at the time of exercising the Currency Exchange Option will be subject to the prevailing laws and regulations. Please note that the new plan after exercising Currency Exchange Option may not have Currency Exchange Option available, and in a worst case scenario, it may only be a one-time option depending on the new plan’s features.

- Your current planned benefit may not be sufficient to meet your future needs since the future cost of living may become higher than they are today due to inflation. Where the actual rate of inflation is higher than expected, you may receive less in real terms even if we meet all of our contractual obligations.

- As the cash value of Reversionary Bonus is non- guaranteed, there may be a risk of overloan when there is adjustment on the cash value of Reversionary Bonus. Immediate loan repayment is required when there is an overloan, otherwise your policy will be terminated and you or the insured may lose the cover.

Key Exclusions to Accidental Death Benefit

Accidental Death Benefit will not cover any conditions that result from any of the following:

- self-destruction while sane or insane, participation in a fight or affray, being under the influence of alcohol or a non-prescribed drug

- war, service in armed forces in time of war or restoration of public order, riot, industrial action, terrorist activity, violation or attempted violation of the law or resistance to arrest

- racing on wheels or horse, scuba diving

- ptomaines or bacterial infection (except pyogenic infection occurring through an accidental cut or wound)

- air travel, including entering, exiting, operating, servicing or being transported by any aerial device or conveyance (except as a passenger of a commercial passenger airline on a regular scheduled passenger trip over its established passenger route)

The above list is for reference only. Please refer to the policy contract of this plan for the complete list and details of exclusions.

Note for Unemployment Benefit

You must be employed under a continuous contract for not less than 24 months and be eligible for a severance payment upon termination under the employment or labour laws of Hong Kong or Macau (according to the place of policy issuance) prior to the involuntary unemployment. Further, such employment cannot be selfemployment, employment by a family member (including spouse, parent, grandparent, child or grandchild) or employment as a domestic servant. The Unemployment Benefit starts on the premium due date at the time when we approve your claim and continues for up to 365 days. Proof of continuous unemployment is required by you upon our request. The Unemployment Benefit is not available if you were informed of your pending involuntary unemployment on or before the issue date or commencement date of the policy, whichever is later.

The Unemployment Benefit will cease on the earliest of the following dates:

- at the end of extended grace period,

- you fail to provide proof of continuous unemployment upon our request,

- the date on which the policy owner has been changed,

- the date on which any claims on waiver of premium under your basic plan is approved,

- at the end of premium payment term of your basic plan,

- the date when any withdrawals or claims of your basic plan and / or add-on plans is made, if the premium payment mode after the payment of benefits is not monthly, and,

- the date when you pay all outstanding premiums.

Claim for Unemployment Benefit must be submitted within 30 days of your involuntary unemployment.

The Unemployment Benefit could only be claimed once per policy and relevant proof is required. The approval of the Unemployment Benefit is subject to our prevailing rules and regulations, and the handling of policy during the extended grace period will be subject to our discretion.

Suicide

If the insured commits suicide within one year from the date on which the policy takes effect, our liability will be limited to the refund of premiums paid (without interest) less any outstanding debt.

After exercising the Change of Insured Option or upon the contingent insured becoming the new insured, if the new insured commits suicide within one year from the effective date of change as recorded by us, our liability will be limited to the refund of premiums paid (without interest) or the sum of guaranteed cash value, cash value of Reversionary Bonus (if any), cash value of Terminal Bonus (if any) and any remaining balance of the Bonus Lock-in Account as at the date the new insured passes away, whichever is higher, less any outstanding debt.

Incontestability

Except for fraud or non-payment of premiums, we will not contest the validity of this policy after it has been in force during the lifetime of the insured for a continuous period of two years from the date on which the policy takes effect. This provision does not apply to any add-on plan providing accident, hospitalisation or disability benefits. After exercising the Change of Insured Option or upon the contingent insured becoming the new insured, such two-year period will be counted again starting from the effective date of change as recorded by us.

Warning Statement and Cancellation Right

Global Power Multi-Currency Plan is an insurance plan with a savings element. Part of the premium pays for the insurance and related costs. If you are not happy with your policy, you have a right to cancel it within the cooling-off period and obtain a refund of any premiums and levy paid. A written notice signed by you should be received by the Customer Service Centre of AIA International Limited at 12/F, AIA Tower, 183 Electric Road, North Point, Hong Kong within the cooling-off period (that is, 21 calendar days immediately following either the day of delivery of the policy or cooling-off notice (informing you/your nominated representative about the availability of the policy and expiry date of the cooling-off period, whichever is earlier). After the expiration of the cooling-off period, if you cancel the policy before the end of the term, the projected total cash value may be substantially less than the total premium you have paid.

Important Notes from the Insurance Agent of The Bank of East Asia, Limited

- The Bank of East Asia, Limited (“BEA”), being registered with the Insurance Authority as a licensed insurance agency, act as an appointed licensed insurance agent for AIA International Limited (incorporated in Bermuda with limited liability) (“AIA”). This insurance plan is a product of AIA but not BEA.

- This insurance plan is underwritten by AIA and it is not a bank savings plan with free life insurance coverage. Part of the premium pays for the insurance and related costs. The premium paid is not a placement of a savings deposit with the bank and hence is not protected by the Deposit Protection Scheme in Hong Kong.

- Add-on plan (if any) is an add-on coverage for this insurance plan with additional premium paid required. BEA does not distribute any add-on plan; therefore, you cannot apply the add-on plan through BEA. If needed, you can contact AIA Customer Service Centre for inquiry after the policy is issued by AIA.

- In respect of an eligible dispute (as defined in the Terms of Reference for the Financial Dispute Resolution Centre in relation to the Financial Dispute Resolution Scheme) arising between BEA and the customer out of the selling process or processing of the related transaction, BEA is required to enter into a Financial Dispute Resolution Scheme process with the customer; however, any dispute over the contractual terms of the product should be resolved between AIA and the customer directly.

- Claims under this insurance plan must be made by you to AIA directly. You can get the appropriate claim form by calling AIA Customer Service Hotline (852) 2232 8968 in Hong Kong or visiting www.aia.com.hk or any AIA Customer Service Centre. For details, please refer to the policy contract provided by AIA.

- BEA’s sales staff (including direct sales staff and authorised agents) are remunerated not only based on their financial performance, but also according to a range of other factors, including their adherence to best practices and their dedication to serving customers’ interests.

- The information you disclosed in response to all AIA’s questions must be true, complete and correct. Failure to disclose true, complete and correct information to AIA may render AIA unable to accept or process your application or the policy void.

- You are reminded to carefully review the relevant product materials provided to you and be advised to seek professional/ independent advice when considered necessary.

- For the benefits and returns mentioned throughout the product brochure and Important Notes, please note that the policy owner is subject to the credit risk of AIA. If the policy owner discontinues and/or surrenders this policy in early policy years, the amount of benefits he/she will get back may be considerably less than the total premiums he/she has paid. Projected and/or potential benefits and/or returns (e.g. reversionary bonus, terminal bonus) presented in the product brochure are not guaranteed and are for illustrative purposes only. The actual future amounts of benefits and/or returns may be lower than or higher than the currently quoted benefits and/or returns.

-

Apart from the key product risks mentioned in product brochure, you are also reminded of the following risks:

1. Liquidity risk – this insurance plan is designed to be held long term. You should only apply for this insurance plan if it is intended to pay the premium for the whole of the premium payment term. If you fail to pay the premium for the whole of the premium payment term, this will cause the policy to lapse or to be terminated earlier than the original benefit term, and the total surrender value (if any) that get back by you may be less than the total premiums paid.2. Risk from surrender – if you cancel the policy before the end of the benefit term, you may suffer a significant loss, and the total surrender value received may be substantially less than the total premiums paid.

3. Non-guaranteed bonus scales – non-guaranteed benefits are based on the bonus scales of AIA determined under current assumed investment return. The actual amount payable may change anytime with the values being higher or lower than those being projected. In other words, a change in the current assumed investment return will affect the reversionary bonus and terminal bonus you will receive. Under some circumstances, the non-guaranteed benefits may be zero.

4. Risk relating to RMB insurance products – The value of RMB is subject to the fluctuation of its exchange rate. There may be exchange rate loss suffered by you due to such fluctuation if you convert RMB into other currencies (including Hong Kong Dollars).

[For personal customer] – RMB is currently not completely freely convertible. Personal customers can be offered to conduct conversion of RMB by the bank using offshore rates and may occasionally not be able to do so fully or immediately as it is subject to the RMB position and market conditions at that time.

[For corporate customer] – RMB is currently not completely freely convertible. Corporate customers can be offered to conduct conversion of RMB by the bank using offshore rates or onshore rates depending on the objective of conversion and may occasionally not be able to conduct fully or immediately as it is subject to the RMB position and market conditions at that time.

You should understand and consider the possible impact on the liquidity of RMB funds. The exchange rate for the offshore RMB market in Hong Kong may be at a premium or discount when compared to the onshore market in People’s Republic of China and there may be significant bid and offer spreads.